|

Review Your Credit Reports to improve your credit to know what might be working in your favor (or against you). This can be done by pulling a copy of your credit report from each of the three major national credit bureaus: Equifax, Experian, and TransUnion. You can do that for free once a year through the official AnnualCreditReport.com website. Then review each report to see what’s helping or hurting your score. Click on the link to gain access to your free annual credit report.

FREE Credit Report Once you obtain your credit report, there are some items that you should pay attention to determine how your credit is being effected (negatively or positively). Some of the simplest items to focus on that can increase your credit scores are incorrectly reported items. Here is a brief list of items to notate. Common Errors to look for:

0 Comments

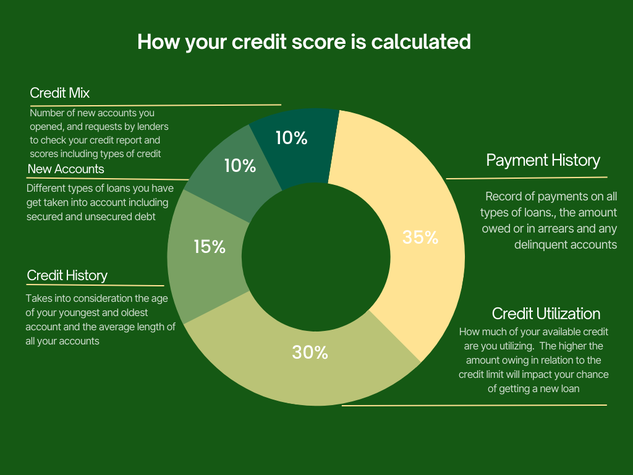

How is your credit score calculated? Your credit score is a three-figure score ranging from 300 – 850 that shows your creditworthiness. Credit scores are calculated using many different pieces of credit data from your credit report. This data is grouped into five categories:

Look for the next series of emails to go much deeper into how your credit scores are calculated, ways to increase and maintain your credit score including do it yourself methods. You are interested in purchasing a home, but your credit score is not high enough to secure a mortgage loan. We have put together a 12 part series of credit tips to assist with improving your scores.

We believe that home ownership is one of the easiest paths to generational wealth. Imagine not renting and not contributing to other people’s wealth at the expense of yours. Imagine paying a monthly mortgage where eventually the money paid can be used to purchase your own rental/investment property. Imagine leaving your property to a loved one that will now always have somewhere to live, can focus on college, or start a business without worrying about paying rent or a mortgage, and can take out an equity loan to help with those same efforts. These are the things that home ownership can do for you and your family, and if you don’t have enough cash to purchase a house outright, you will need a loan. One of the most important components of securing a loan is to give the loan issuer the confidence that you will pay it back as agreed and this confidence is gained through your credit history. Banks and other mortgage lenders will review your credit profile in order to assess the risks involved with extending a loan to you. Simply put you will be judged by your credit score, therefore it is very important that you understand how it all works. Through this 12 part series of credit tips you will find that there’s multiple things you can do on your own to improve your score. Let's get started. Credit is part of your financial power. It helps you to get the things you need now, like a loan for a car, a credit card, furniture, appliances, etc. and these loans are based on your promise to pay later. Working to improve your credit helps ensure you'll qualify for loans when you need them. Having good credit essentially means that you are making regular payments on time on each of your accounts until your balance is paid in full. Alternatively, bad credit states you have had a hard time holding up your end of the bargain; you may not have paid the full minimum payments or made those payments on time. You will find it useful to know how you are managing your credit impacts your credit score. |

|

|

Proudly powered by Weebly

|